EXPOSED: The 2026 "Debt Loophole" US Homeowners Are Using To Escape The Minimum Payment Trap Forever

Stop throwing your hard-earned equity away on credit card interest. An investigative report reveals how thousands are legally slashing their unsecured debt without refinancing or losing their homes.

The American Dream of homeownership has quietly turned into a financial nightmare for millions. While inflation reports in 2026 claim the economy is stabilizing, the reality on Main Street tells a much darker story. Property taxes have skyrocketed, grocery bills remain painfully high, and utility costs are draining middle-class bank accounts. To keep their heads above water, hard-working Americans have been forced to rely on credit cards just to survive.

The result? A staggering $1.3 trillion in nationwide credit card debt. But the real crisis isn't just the debt itself—it is the predatory "Minimum Payment Trap."

The Silent Wealth Killer

If you have a $20,000 credit card balance at the current 2026 average interest rate of 24.5%, making only the minimum payment means you will be in debt for over 28 years. Worse, you will end up paying back more than $30,000 in pure interest. The banks know exactly what they are doing. They design these minimums to keep you on a perpetual hamster wheel, quietly siphoning away the wealth you should be building in your home.

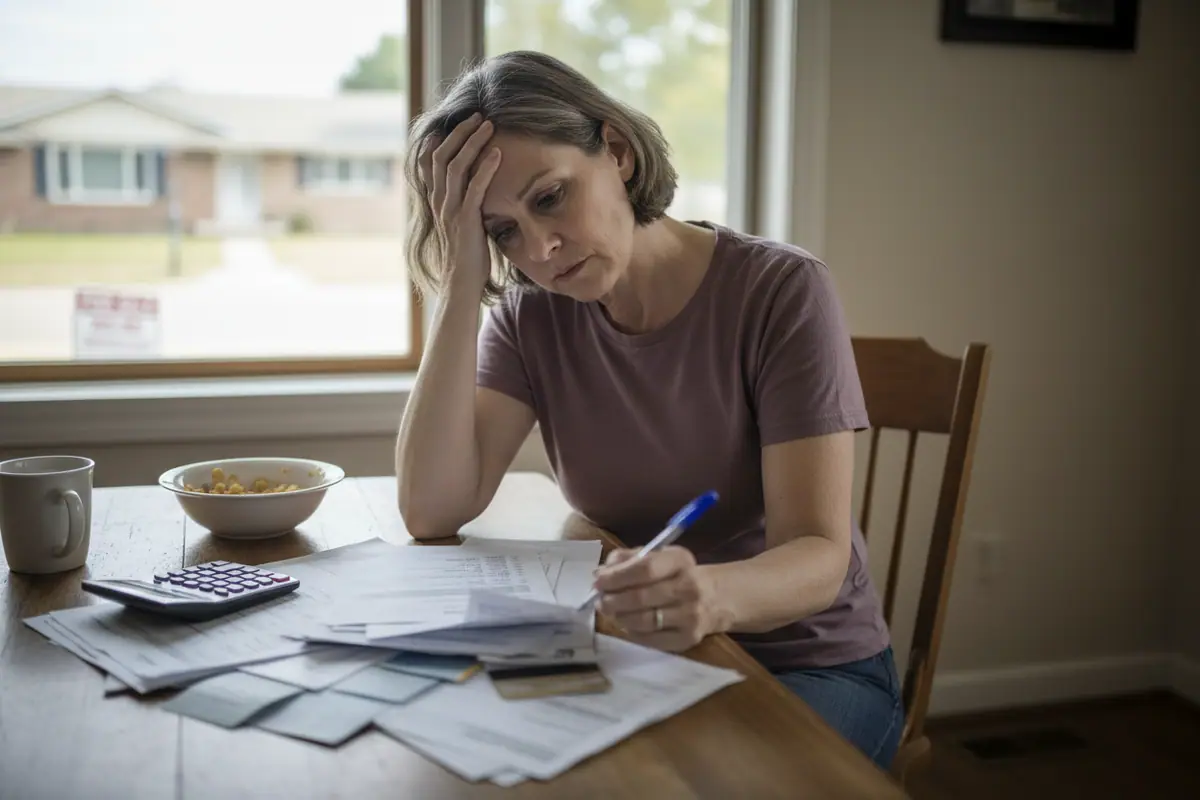

Take Mark Jenkins, a 44-year-old homeowner from Columbus, Ohio. Two years ago, Mark had to replace his roof and cover unexpected medical bills. He put it all on plastic, assuming he would pay it off quickly. Fast forward to early 2026, and Mark was drowning.

"I was literally sitting at my kitchen table, crying over a mountain of credit card bills," Mark confessed. "I had $38,000 in debt across four cards. I was paying $900 a month in minimums, but the balances weren't moving. I was terrified I would have to sell my house just to pay off Visa and Mastercard."

A Skeptical Discovery

Mark was desperate. He tried looking into a Home Equity Line of Credit (HELOC), but with 2026 interest rates still punishingly high, borrowing against his house felt like financial suicide. That is when a coworker mentioned a little-known financial strategy facilitated by a company called National Debt Relief.

Mark was immediately suspicious. "I thought it was an absolute scam," he told us. "Whenever you hear about debt relief, you assume they are going to put a lien on your house, destroy your life, or steal your identity. I ignored it for weeks."

But as the late fees piled up, Mark finally caved and made a phone call. What he discovered wasn't a scam, but a completely legal, highly regulated debt resolution framework that forces aggressive creditors to the negotiating table. Today, Mark is a different man. He spends his mornings sipping coffee on his porch, relaxed, looking at a customized debt resolution plan on his phone that has him entirely debt-free in a fraction of the time.

The Editorial Investigation

As a consumer finance investigative journalist, my inbox is flooded daily with "miracle" financial cures. Ninety-nine percent of them are predatory garbage designed to exploit vulnerable people. But the sheer volume of verified success stories surrounding National Debt Relief in 2026 made me stop and take notice.

I needed to know if this was a legitimate lifeline for homeowners or just another clever trap. The only way to find out was to test it from the inside.

I couldn't just use editorial funds for this; I needed real debt. I approached our associate producer, Emily, a 39-year-old homeowner who had confidentially shared her struggles with $26,500 in high-interest credit card debt. She was losing sleep, constantly stressed, and trapped in the exact minimum payment cycle we were investigating. I asked if she would be willing to enroll in National Debt Relief and document every single step of the process for our readers.

She agreed, though she was incredibly nervous. We set up her consultation, and the live test began.

Day 1

Emily completed her initial consultation. "I was shocked that the call was completely free," she reported. "The advisor was empathetic and didn't judge me at all. They reviewed my debts and confirmed I qualified. The scariest part was when they instructed me to stop paying my credit card companies directly and instead redirect those funds into a special, FDIC-insured dedicated account that I control. It felt wrong, almost like I was breaking the rules, but they explained this is the leverage needed to force the banks to negotiate."

Day 3

The reality of the program started to set in. "I logged into my National Debt Relief dashboard this morning. It is incredibly transparent. I can see exactly how much money is accumulating in my dedicated account. The constant harassing phone calls from creditors have started, but National Debt Relief gave me exact instructions on how to handle them and route them to their legal team. For the first time in three years, I feel like I have a shield between me and the banks. I saw my customized resolution plan today—it cuts my projected payoff time from 22 years down to just 28 months."

Day 7

A massive breakthrough. "I woke up to an alert on my phone. National Debt Relief had already reached their first settlement with my highest-interest card. A $8,500 balance was negotiated down to a fraction of what I owed. I authorized the settlement with a single click. The relief I felt was physical—like a crushing weight had been lifted off my chest. I am no longer throwing money into a black hole of interest. I am actually seeing the light at the end of the tunnel."

Emily did not just clear a massive chunk of her debt; she reclaimed her life. By breaking free from the minimum payment trap, she freed up hundreds of dollars a month in cash flow. She didn't have to take out a dangerous second mortgage, and her home equity remains completely untouched and safe. Last week, she used her newfound financial breathing room to book a modest weekend getaway with her kids—something she hadn't been able to afford since 2023. Mark, our homeowner from Ohio, is experiencing the exact same peace of mind. He is no longer crying over bills; he is planning for his retirement again.

The economic landscape of 2026 is unforgiving. Banks are tightening their belts, and credit card companies are becoming more aggressive with their interest rate hikes. If you are a homeowner sitting on a mountain of unsecured debt, waiting will only cost you more money and put your financial security at greater risk. The window to utilize these aggressive negotiation tactics is open right now, but as more consumers catch on, banks may begin lobbying to close these consumer-friendly loopholes.

After a rigorous investigation and a real-world stress test, our editorial verdict is clear. National Debt Relief is not only legitimate, but it is also one of the most effective, ethical, and powerful tools available for Americans who are serious about escaping the minimum payment trap. It requires discipline, but the reward is true financial freedom. If you are tired of enriching the banks while your own bank account drains, it is time to take your power back.

Accelerated Debt Freedom

Resolve high-interest credit card debt in a fraction of the time it takes by making minimum payments.

Protect Your Home Equity

Achieve financial relief without resorting to risky HELOCs or borrowing against your property.

Lower Monthly Burden

Consolidate your debt obligations into one manageable monthly deposit that fits your actual budget.

Stop Wasting Money on Interest

Force creditors to negotiate the principal balance, stopping the endless cycle of compounding APRs.

Zero Upfront Fees

You pay absolutely nothing until a settlement is successfully reached and you agree to the terms.

FAQ

Does enrolling in this program put my home at risk?

Absolutely not. National Debt Relief specializes in unsecured debt (like credit cards and medical bills). Because these debts are not tied to an asset, your home, car, and property are completely safe and are not used as collateral.

Will I have to pay expensive upfront fees to get started?

No. By law, legitimate debt resolution companies cannot charge you upfront fees. National Debt Relief only collects a fee after they have successfully negotiated a settlement, you have approved it, and at least one payment has been made toward that settlement.

Is this just another loan to pay off my current loans?

No, this is not a loan. You are not taking on new debt to pay off old debt. This is a debt resolution program where experts negotiate with your creditors to reduce the total amount you owe, allowing you to pay off the agreed-upon lower balance.

Will this impact my credit score?

Yes, initially. Because you are redirecting payments into a dedicated account rather than paying the creditors directly, your credit score will temporarily drop. However, as your debts are settled and cleared, your debt-to-income ratio improves dramatically, which is a major factor in rebuilding a healthy financial profile long-term.

Comments

I keep seeing ads for debt relief, but I'm incredibly skeptical. Has anyone actually used this specific program? I don't want to get scammed out of what little money I have left.

@Thomas Henderson I was exactly like you. Thought it was a total scam. But I used National Debt Relief last year when my Visa hit $18k. It took about 24 months, but I am completely debt-free now. They are legit, just read the fine print and follow their instructions.

I just signed up for my free consultation. I have been paying $600 a month in minimums and my balance has literally only gone down by $40 in six months. I can't live like this anymore. Praying this works.

Does anyone know what percentage they actually take as a fee? I know it says no upfront fees, but they have to make money somehow. Just trying to do the math before I call.

@Robert Miller The fee varies depending on your state and total debt, but it's usually between 15% to 25% of your enrolled debt. But honestly, even with the fee, I saved thousands compared to the crazy 26% interest the bank was charging me.

Quick question regarding the dedicated account. Do I have access to those funds, or does the company hold my money? I want to make sure I'm in control.

This article hits so close to home. Between my mortgage and the cost of groceries right now, I've had to put all my classroom supplies and gas on my credit card. I feel like I'm drowning. Calling them on my lunch break today.

Just wanted to post an update! Month 4 in the program and they just settled my Discover card for 45% of what I owed. My credit took a hit, but honestly, the relief of not having that $12,000 hanging over my head is worth it.

I've been on the fence about this for weeks. I'm so scared of ruining my credit score, but I also know I'll never pay off this $30k at this rate. Reading these comments is giving me a little courage.

@Jason K. That is amazing to hear! I just saw on the news that banks are getting stricter with hardship programs this year. I'm not waiting any longer, going to fill out the form now before they close this loophole.

Best decision I ever made. Kept my land, kept my house, and got rid of $42,000 in unsecured debt. The collection calls were annoying for the first few months, but you just have to trust the process. Stay strong folks.

Leave a comment